How to Use the Capital Requirement Module

Access the ORM system, and navigate to the “Capital Requirement” module to begin the process.

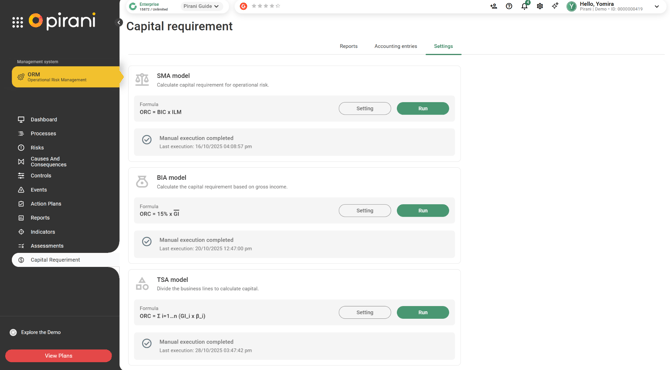

Capital Requirement Model Configuration

When you access “Capital Requirement” in the “Settings” tab, you will be able to select and configure the model or models you wish to use.

Available Models

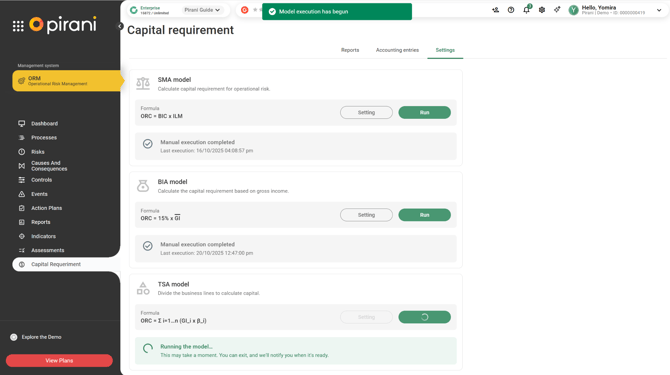

- SMA Model – Standardized Measurement Approach

- BIA Model – Basic Indicator Approach

- TSA Model – The Standardized Approach

SMA – Standardized Measurement Approach

In the “SMA Model Parameters” Section

You will find a configuration form, along with a “More Information” option where you can access detailed explanations of all key terms.

Currency

In Pirani, regional settings — including the default currency — are defined at the organization level.

If you need to change the currency, go to Organization Settings > Configuration.

Magnitude

The magnitude setting helps present data in a more organized and readable way within the interface.

It allows you to scale numerical values according to the size and complexity of your organization.

Type of Time Window

Depending on each country’s regulations, the calculation does not always use the full calendar year. Instead, time windows may be defined according to the type of analysis required.

Below are the available options:

Fixed Window

Performs an analysis based on full years, always from January 1 to December 31, using the last 5 available years.

It is a static window and does not depend on the date selected by the user.

Rolling Window

Performs the analysis using an interval that adjusts dynamically according to the selected start date.

The window shifts (“moves”) as you change the reference date.

Count Backward from a Reference Date

Allows you to define a specific retrospective range using the selected date as the starting point.

Example:

If the reference date is November 2025 and you need a 3-year window, the system will take the period from November 2022 to November 2025.

ILDC Component Calculation Model

There are two methods available to calculate the Interest, Leases, and Dividends Component (ILDC).

Simple Method Option

The Simple method does not require any additional parameters.

With Cap on Earned Assets

The With Cap on Earned Assets method requires an additional parameter called the Adjustment Factor.

Users can adjust this factor as needed. By default, it is set to 0.0225, the value recommended by Basel IV.

This adjustment factor places a limit on the impact of earned assets in the calculation, ensuring compliance with regulatory standards.

BIC (Business Indicator Component) Calculation Method

This method defines the Business Indicator (BI) tranches and their corresponding marginal coefficients used to calculate the Business Indicator Component (BIC).

You can configure it by:

Flat rate per bracket

You can modify the brackets, and by default, there are predefined associated values. Additionally, your organization can customize these settings based on local regulatory requirements.

If the BI falls within any of the defined brackets, it is multiplied by the respective percentage (%) shown in the table, resulting in the calculated BIC.

Tiered Marginal Rate

In this case, the table will display the formulas.

If any value is adjusted, the formulas will automatically update accordingly, as the calculations depend on those values.

Why Are There Two Options?

These two options are available because regulatory approaches may vary by country.

It is common to use the Flat Rate per Bracket method during the transition phase.

Once the transition period ends, institutions typically switch to the Tiered Marginal Rate method, which reflects the finalized regulatory requirements.

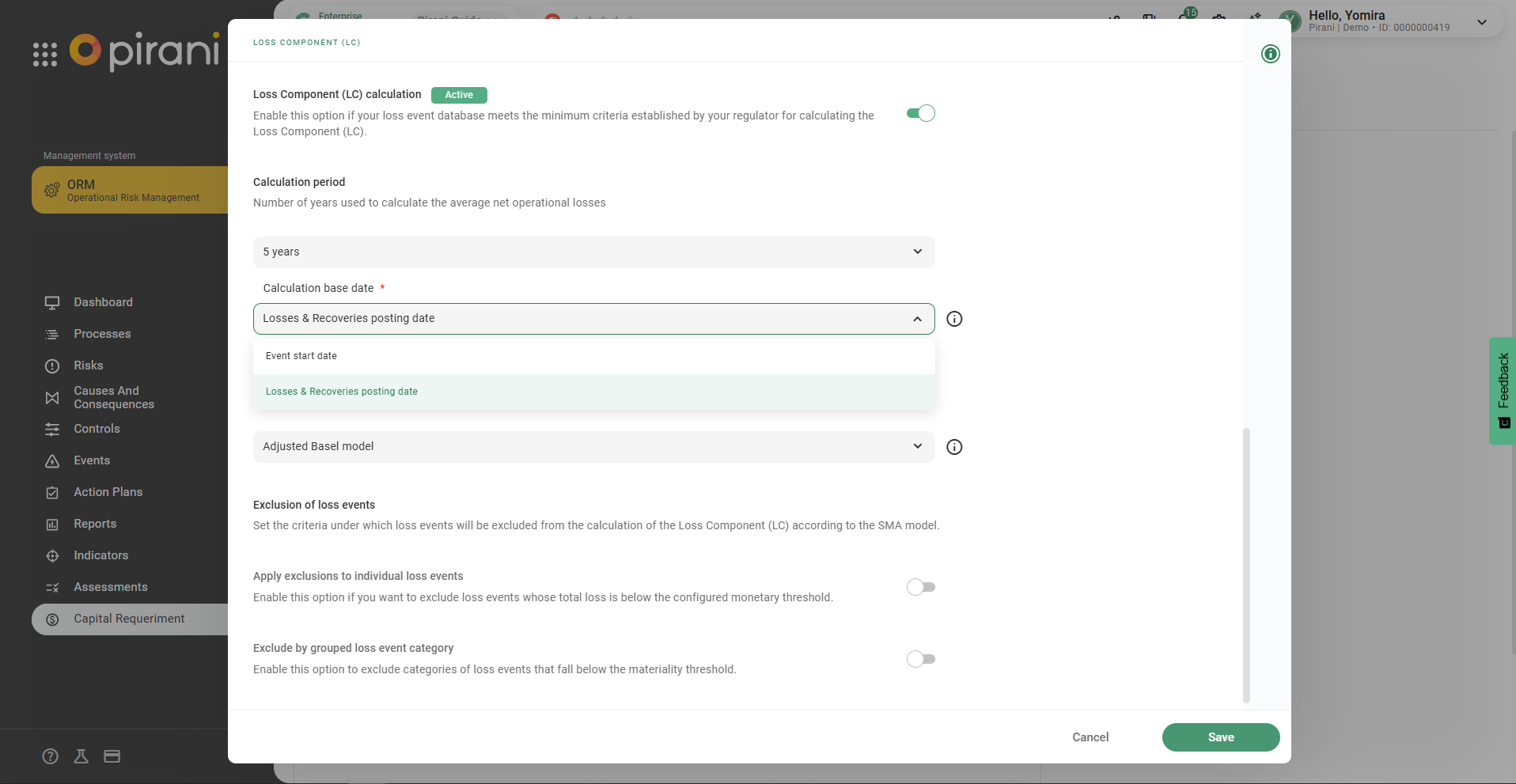

How Does the Loss Component (LC) Work?

The Loss Component (LC) allows institutions to incorporate historical data from operational loss events to reduce or offset the capital requirement.

Important:

Activating this component can lower your capital requirement, only if the loss data meets the quality standards required by regulatory authorities.

When Should You Activate or Deactivate the Loss Component?

|

Organization Status |

Recommendation |

|

✔️ You have a complete loss event history (minimum of 5 to 10 years), audited and certified by the relevant regulatory authority. |

Activate the LC component to benefit from capital mitigation based on real, validated data. |

|

❌ You are in a transition phase and do not yet have sufficient or certified data. |

Keep the LC component deactivated until you meet the required conditions. |

Requirements to Activate the Loss Component

For loss events to be valid and usable in the LC calculation, they must meet the following criteria:

- Sufficient Historical Data:

- At least 5 years of operational loss events during the transition phase.

- At least 10 years after the transition phase is complete.

- At least 5 years of operational loss events during the transition phase.

- Quality Certification:

Data must be audited and certified by your country’s regulatory authority. - Clear and Accurate Classification:

- Events must be classified in accordance with Basel categories.

- Start and end dates must be clearly recorded and controlled.

- Losses must be linked to the appropriate accounting records.

- Data must be complete, consistent, and up to date.

- Events must be classified in accordance with Basel categories.

Why Is It Important?

The loss component allows you to incorporate your organization’s actual data to calculate the Loss Indicator (ILM). A certified ILM can reduce the capital requirement, but only if the information used is reliable, audited, and compliant with regulatory standards.

Recommendation

Enable this component only when:

- Your events are properly recorded.

- They have supporting documentation.

- They are audited and certified.

- They are recognized by your regulatory authority.

Until these conditions are met, you may keep it disabled while you work on consolidating and certifying your data.

Calculation Base Date:

- Event Start Date: The calculation will use the date entered in the event’s start date field.

- Loss and Recovery Posting Date: The system will consider the dates of losses and recoveries associated with those events.

How Does the Internal Loss Multiplier (ILM) Calculation Model Work?

There are three models available for ILM calculation:

- Basel Model: This is the primary model, and the calculation is performed using the following formula:

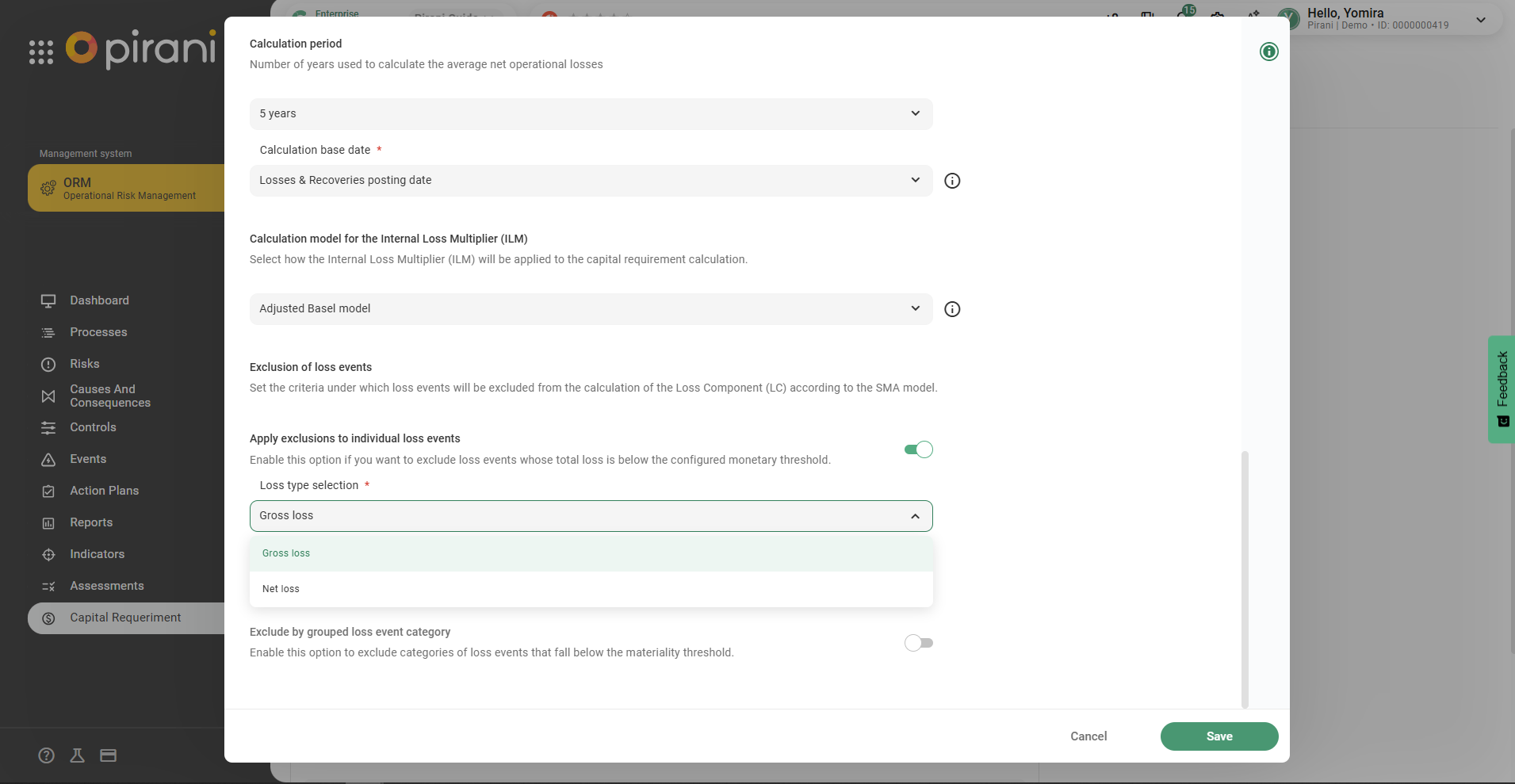

Adjusted Basel Model: This model uses the same formula as the Basel Model, but applies adjustments based on the number of decimal places, depending on system or regulatory requirements.

Fixed ILM Value :This model applies when an organization does not yet have all the required loss data.

A fixed ILM value—typically 1.5—is used with regulatory approval, often in countries where the loss component calculation is not yet fully defined or implemented.

How Do Loss Event Exclusions Work?

Basel IV, and specifically its implementation in countries such as Colombia, allows institutions to optionally exclude certain operational loss events from the Loss Component (LC) calculation.

This means it is not mandatory to include all recorded events from the past 5 or 10 years. Instead, institutions may choose to include only those events that are material and relevant, based on criteria established by local regulations.

💡 While including all events offers a more comprehensive analysis, Basel acknowledges that excluding minor events can reduce statistical distortions and improve the quality of the calculation.

This flexibility allows organizations to:

- Apply materiality and relevance criteria.

- Adjust their capital model based on the maturity and quality of available data.

- Comply with local regulatory frameworks without compromising the soundness of the calculation.

Exclusion Methods

There are two available methods for excluding loss events:

1. Apply exclusions to individual loss events

This functionality allows you to automatically exclude individual operational loss events whose value falls below a minimum materiality threshold. It also allows you to choose whether the exclusion is based on the gross loss or the net loss.

✅ Only events that exceed the established threshold will be considered in the calculation.

How Does It Work?

Once this option is activated, the system will:

- Review each individual recorded loss event.

- Exclude from the Loss Component calculation all events whose loss amount is below the defined threshold.

- Include only events equal to or greater than the threshold in the final calculation.

When Should You Activate This Option?

Activate this option if you want to:

- Exclude immaterial losses from the Loss Component calculation.

- Align your analysis with materiality criteria defined by Basel IV.

- Comply with best practices recommended by local regulatory authorities.

⚠️ Considerations

- This type of exclusion is allowed under Basel IV and is commonly used as part of the SMA model in various jurisdictions.

The threshold must be properly documented and justified in your internal methodology, or validated by the relevant regulatory authority.

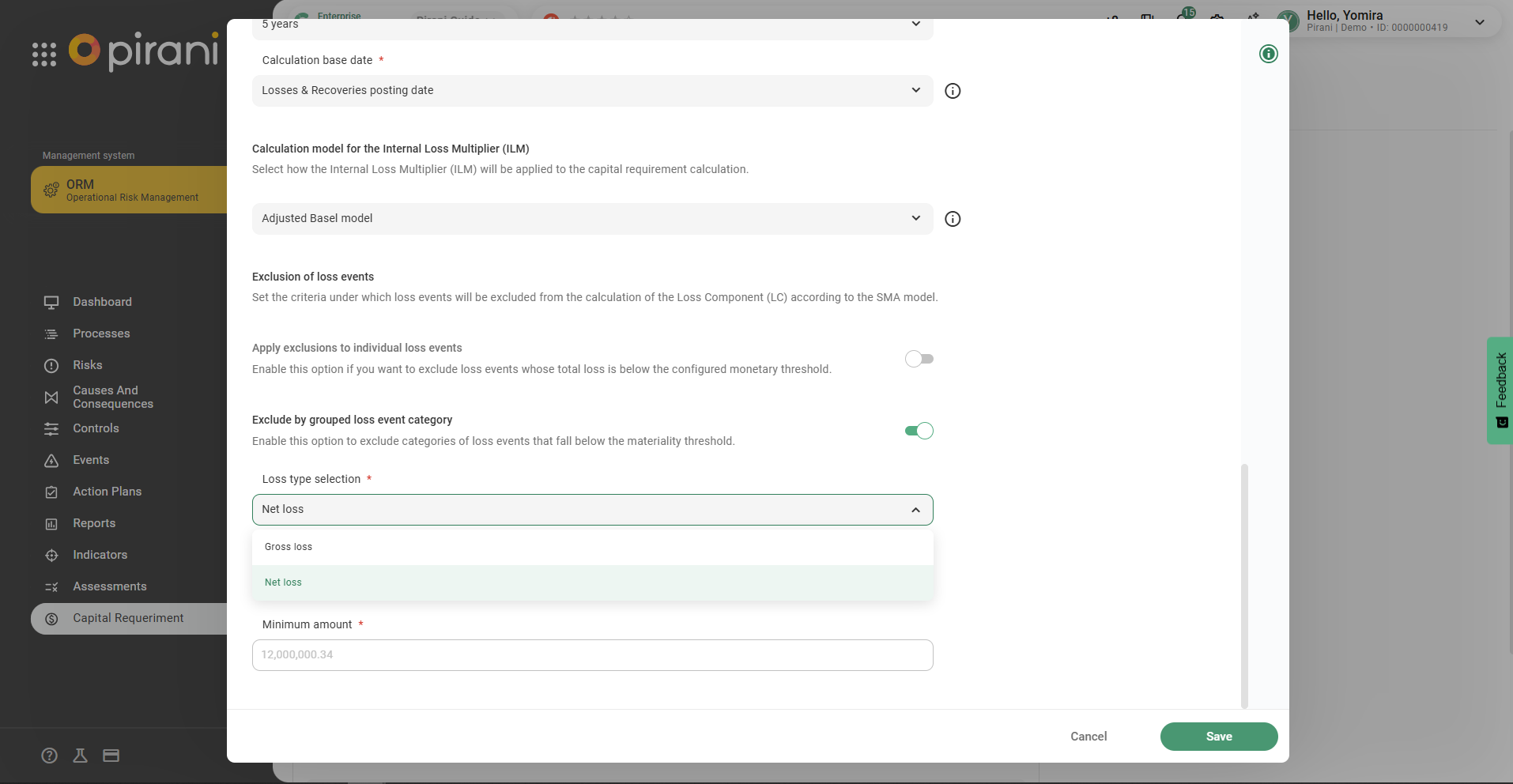

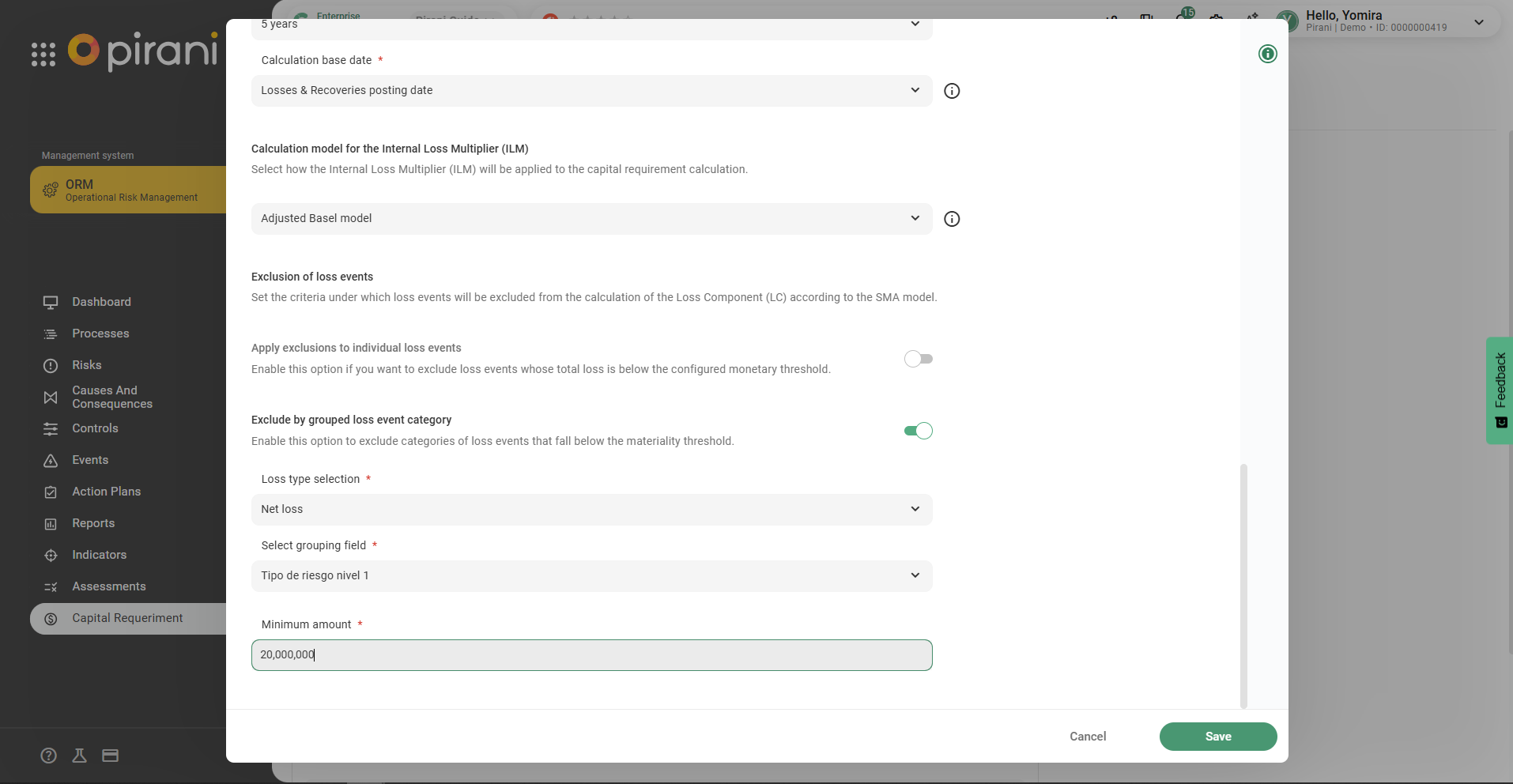

2.Exclude by grouped loss event category

This option allows you to exclude from the Loss Component (LC) calculation any loss event categories (e.g., Basel categories) that do not exceed a defined materiality threshold.

The system groups events based on a dynamic field (such as Basel category), sums the total losses per group, and automatically excludes the entire category if its total losses fall below the defined threshold.

How Does It Work?

- Select the dynamic grouping field

- Example: Basel Category

- Example: Basel Category

- The system groups events by the selected category

- It sums the total losses within each group

- It applies the exclusion condition:

- If the total losses for a given category are below the defined threshold (e.g., $20,000,000):

❌ Events in that category are excluded from the LC calculation. - If the total losses exceed the threshold:

✅ Events in that category are included in the calculation.

- If the total losses for a given category are below the defined threshold (e.g., $20,000,000):

When Should You Activate This Option?

Enable this option if you want to apply an automatic materiality-based exclusion using the aggregated sum of losses by category, and also select the type of loss (gross or net) you want to use for that exclusion.

It is particularly useful for:

- Reducing the impact of minor events

- Avoiding distortions in the Loss Component (LC) calculation

- Complying with Basel IV–recognized criteria

🔎 Note:

This methodology is endorsed by Basel and is currently applied in Colombia as part of recognized regulatory best practices.

Practical Example

Selected grouping field: Basel Category

- Category A – Total loss amount: $25,000,000 → ✔️ Included in the calculation

- Category B – Total loss amount: $18,000,000 → ❌ Excluded from the calculation

Considerations

- The minimum threshold may vary depending on local regulations or your organization’s internal policies.

- This exclusion does not delete the events; it simply omits them from the LC calculation if the total per category does not meet the defined threshold.

In the “Accounting Entries” tab, remember:

Ensure that the chart of accounts master data and the classifications of “accounting items” are properly configured.

Consult our Help Center for more information.

This step applies to the SMA model (Standardized Measurement Approach) with the loss component.

You must confirm that your loss event database is aligned with the applicable regulatory guidelines and meets the required quality standards for use in the capital requirement calculation.

📌 Reminder:

Loss events must be certified for the calculation under the SMA model to be executed properly and in accordance with regulatory standards.

Pirani supports you in the event certification process.

If you need help, consult our Help Center.

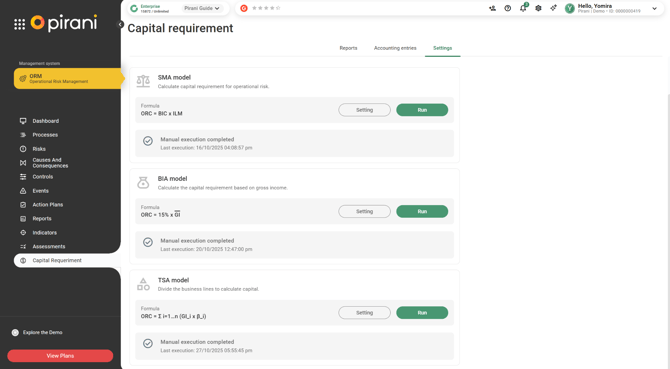

Return to the “Configuration” tab to run your models.

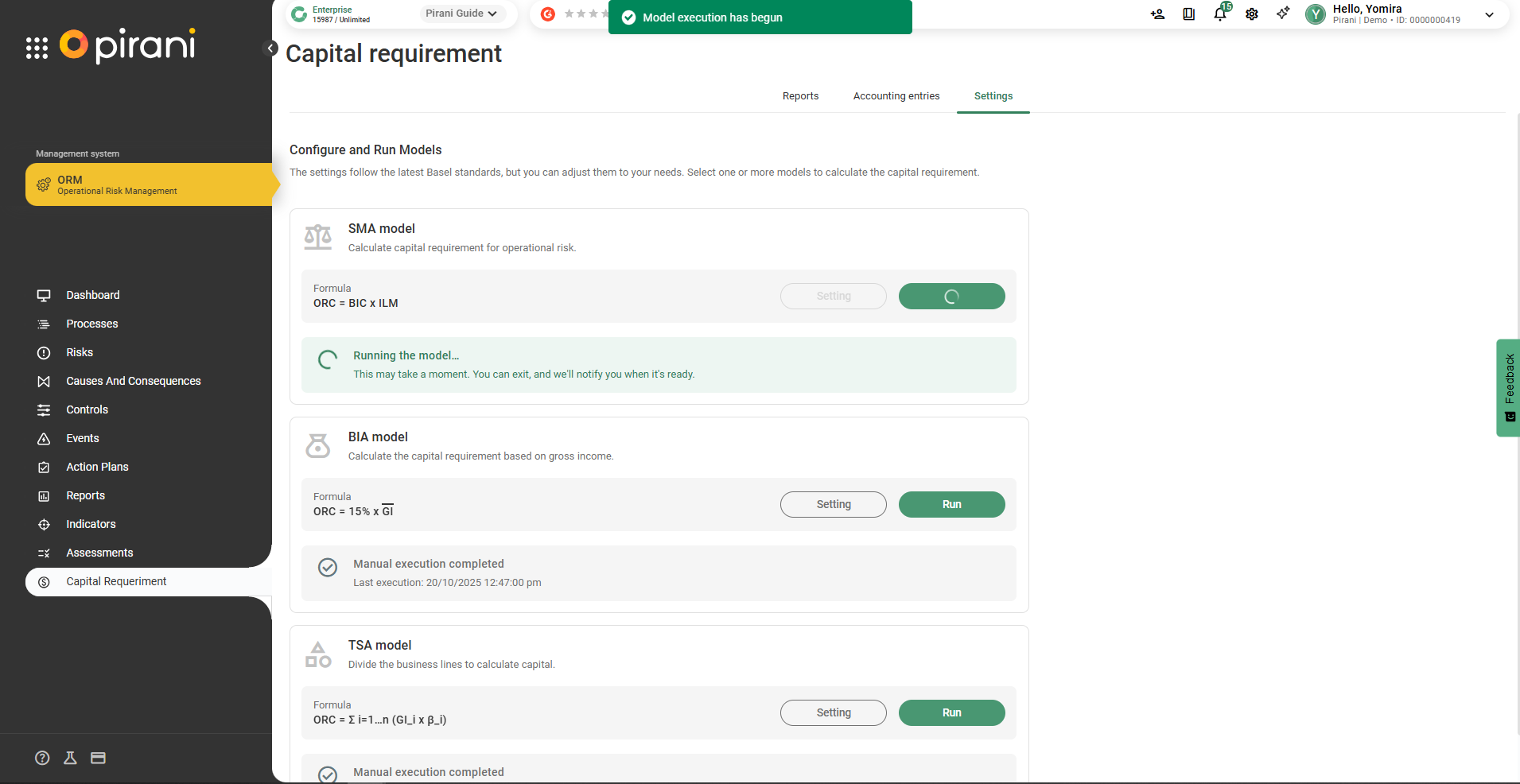

Steps for execution:

Once the “running model” process begins, the system will temporarily restrict access to the following modules:

- Events: You will not be able to make adjustments or modifications during execution.

- Accounting Entries: This module will also be locked until the execution is complete.

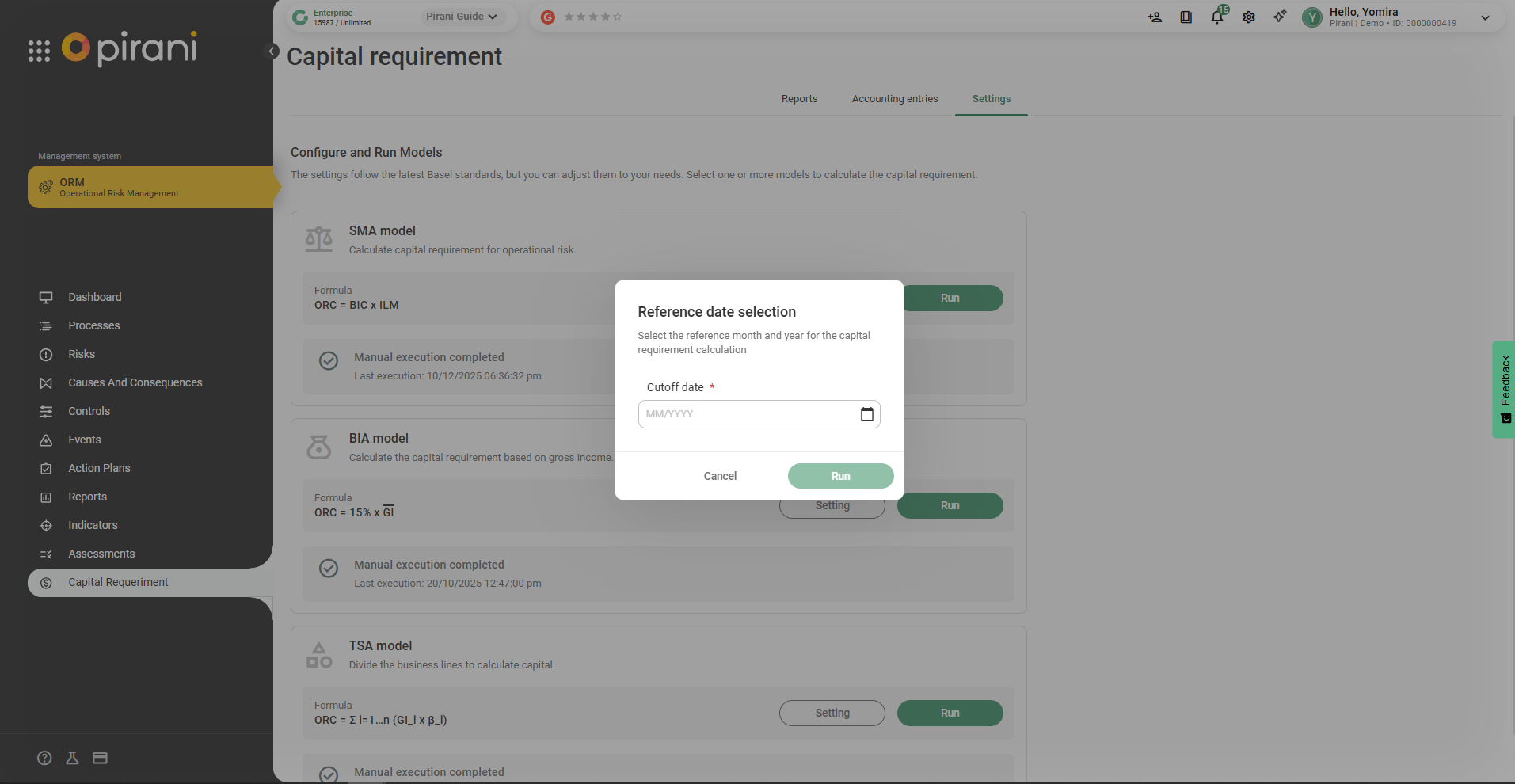

Reference Date Selection

Cut-off Date

Allows you to choose the reference month and year for the capital requirement calculation.

Once the date is selected, the system will display a description of the time range that will be used to perform the calculation.

⚠️ Important: Make sure all necessary adjustments have been completed before running the model.

The “model was manually adjusted” status indicates that, upon execution, the model was completed.

The system formally closes the process and records the results as final.

Important:

Once finalized, the system automatically stores the date and time of the last execution, allowing you to maintain a historical record for traceability, audit, and future validation purposes.

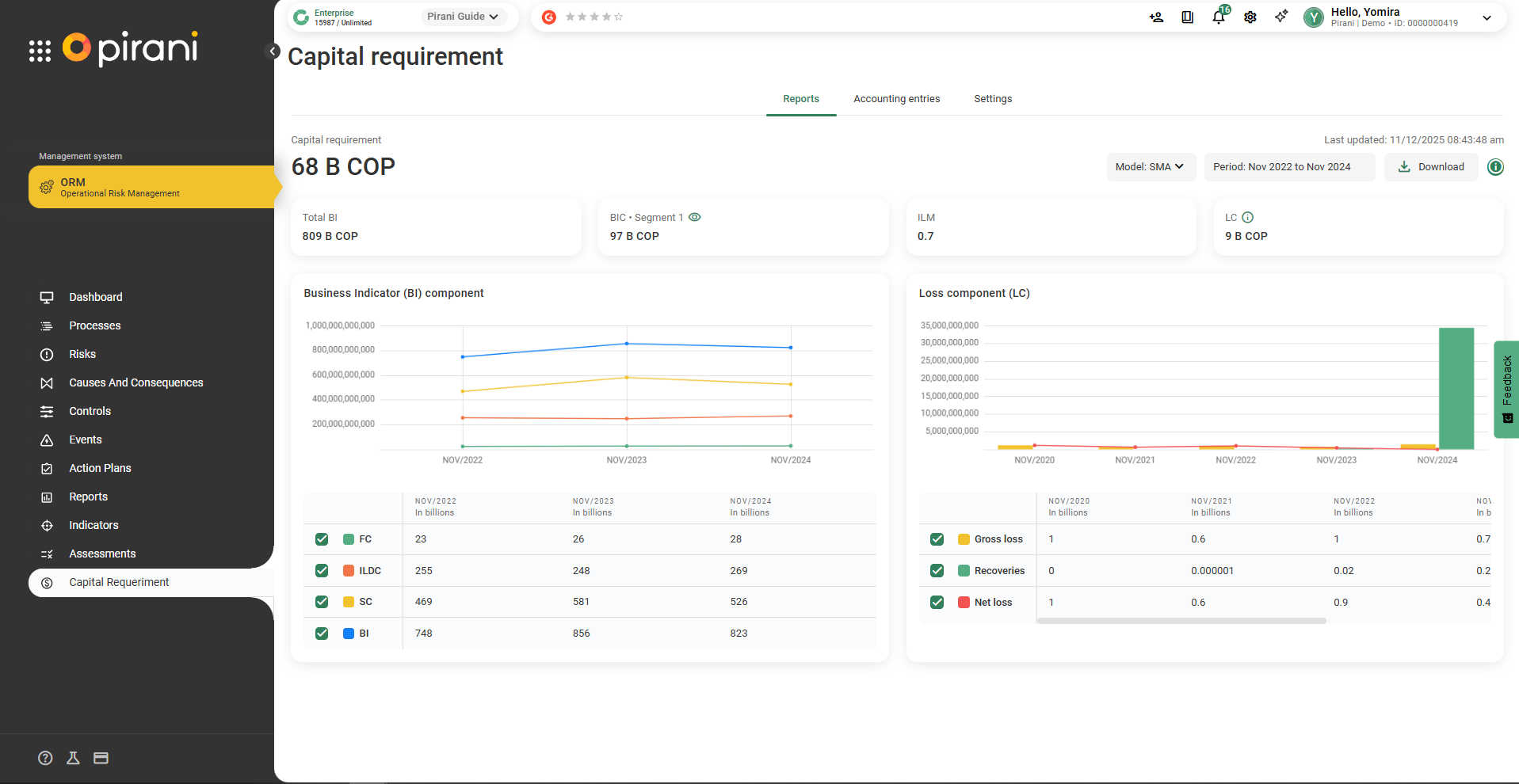

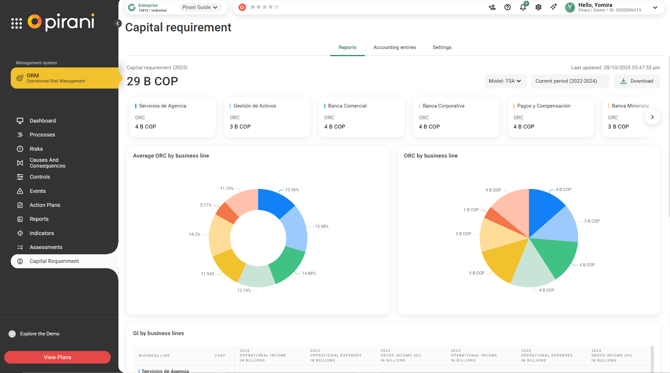

Once finalized, you can go to the “Reports” section after the calculation has been executed, to view the results and download the information, where:

- The Business Indicator Component will always be calculated based on the last three years.

- The Loss Component will be considered over a period of five to ten years, depending on the transition phase and data availability.

In addition, by interacting with the report chart, you’ll be able to view in detail the accounting entries associated with each period.

BIA Model (Basic Indicator Approach) (Basel II)

The BIA (Basic Indicator Approach) model, defined by Basel II, is the simplest method for calculating the capital requirement for operational risk.

It is based on a single indicator: the average gross income over the last 3 years.

Capital Requirement (ORC) = 15% x Average Gross Income (3 years)

Go to the "Settings" tab.

BIA Model Parameters

Currency:

In Pirani, there is a regional settings option under Organizations where the currency is defined at the organizational level. If you wish to change it, go to “Settings” under Organizations.

Magnitude:

This parameter aims to make data visualization more organized within the interface. It adapts according to the magnitudes handled, depending on the size of the organization.

Gross Income Calculation

Coefficient Value

Coefficient:

A percentage between 0 and 100 used in the capital calculation to adjust the organization's exposure to operational risk.

Related Accounting Items

Operating Income

Depending on the model you wish to configure, you can select the variables available and evaluate them based on the transactions associated with those accounting items.

Operating Expenses

Includes associated operating expenses necessary to adjust the capital requirement calculation.

Exclude Years with Zero or Negative Gross Income (GI)

Enable this option to automatically exclude years in which the Gross Income (GI) was zero or negative.

Save Your BIA Configuration and Run Your Model

Steps for Execution:

Once the “Running the model” process begins, the system will temporarily restrict access to the following modules:

- Accounting Transactions: This module will also be locked until the execution is complete.

* Important:

Make sure all necessary settings are completed before running the model.

The status "The model was adjusted manually" indicates that the model was successfully executed, the system formally closes the process, and the results are recorded as final.

Note:

At the end of the execution, the system automatically stores the date and time of the last run. This allows for maintaining a historical record for traceability, auditing, and future validation purposes.

Once Finished, You Can Go to the “Reports” Tab.

After running the calculation, you can view the results and download the information, where:

- The Business Component will always be calculated based on the last three years.

Additionally, by interacting with the report chart, you will be able to view in detail the accounting transactions associated with each period.

TSA Model (The Standardized Approach)

It is a method used to calculate the capital requirement for operational risk that assigns a fixed percentage of capital to different business lines, based on the gross income of each. This approach allows a more accurate reflection of each area’s exposure to risk, balancing simplicity and risk sensitivity compared to the Basic Indicator Approach (BIA).

Go to the “Configuration” tab.

TSA Model Parameters

Currency: In Pirani, there is a regional configuration within Organizations, where it is defined at the organization level. If you wish to change it, go to “Settings” in Organizations.

Magnitude: Its purpose is to make data visualization more organized in the interface, according to the scales handled depending on the size of the organization.

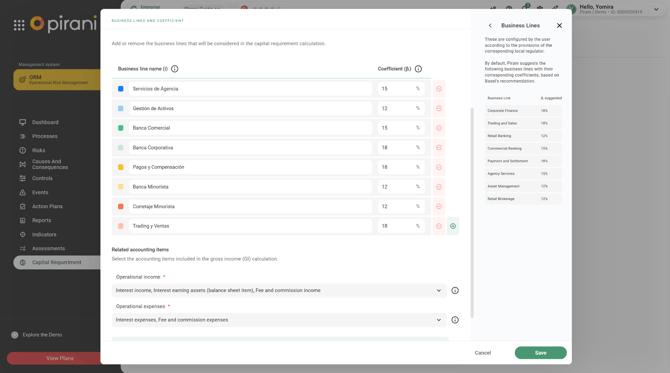

Business Lines and Coefficient

Why are business lines added or removed?

This occurs for three main reasons:

If a business line has negative gross income in a given year, it is taken as zero for that year (it is not subtracted).

If a line has negative income for all three years, it is not included in the calculation.

Example:

If the “Trading and Sales” line had losses every year → it is removed from the summation.

b) Bank restructuring

If the bank creates or eliminates business units (for example, merges “Commercial Banking” and “Retail Banking”), the lines must be regrouped to reflect the current structure.

This may involve adding or removing business lines from the TSA model.

c) Regulatory compliance

Some jurisdictions allow the exclusion of lines that do not represent material activities or if their information is not sufficiently reliable.

This avoids distorting the capital calculation.

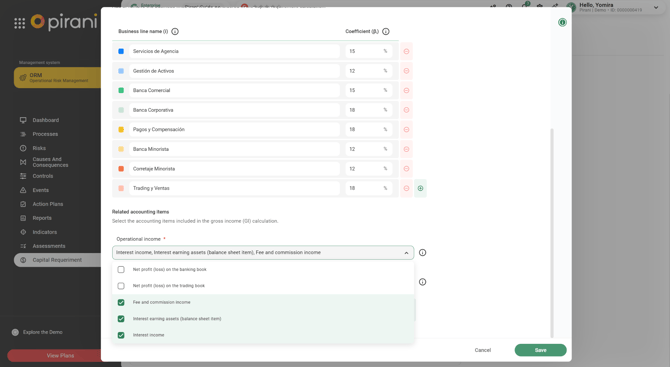

Related Accounting Items

Operational Income

According to the model you wish to configure, you can select the variables that exist and evaluate them based on the movements associated with those “accounting items.”

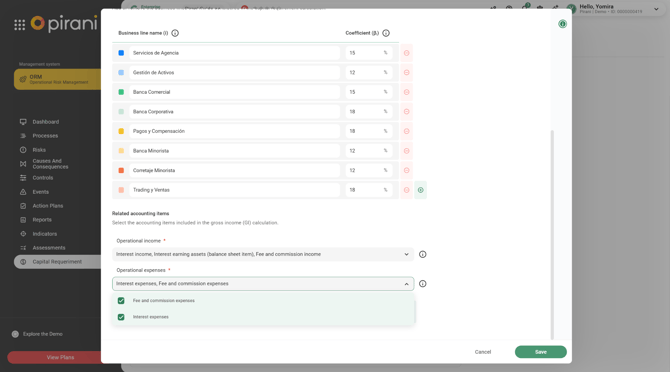

Operational Expenses

Includes associated operational expenses necessary to adjust the capital requirement calculation.

Important: Negative GI values per business line and year are adjusted to zero, preventing negative values in the capital requirement calculation.

Save your TSA parameterization and run your model.

Execution steps:

Once the “Running model” process starts, the system will temporarily restrict access to the following modules:

Accounting Movements: This will also remain blocked until the execution finishes.

Important: Make sure you have completed all necessary adjustments before running the model.

The status “the model was manually adjusted” indicates that once executed, the model was completed, the system formally closes the process, and the results are recorded as final.

Upon completion, the system automatically stores the date and time of the last execution, allowing you to maintain a historical record for traceability, auditing, and future validation purposes.

After finishing, you can go to the “Reports” tab. Once the calculation is executed, you can view the results and download the information, where:

The Business Component will always be calculated based on the last three years.

Additionally, when interacting with the report graph, you can view in detail the accounting movements associated with each period.

Get to Know Key Terms Before or After Using the Module

What Are Events, and Why Is It Important to Record Them?

Risk events are situations that may cause economic losses, legal consequences, or damage to your organization’s reputation. These can include operational errors, fraud, technology failures, among others.

Recording these events not only enables internal tracking and management, but is also crucial to computing the Operational Risk Capital Requirement as defined under Basel III.

⚠️ Only events that are recorded, verified, and certified in accordance with each country’s regulations can be considered valid in the calculation.

With Pirani you can:

- Report events collaboratively across the organization

- Create and update events manually or in bulk

- Ensure traceability and data quality necessary to meet regulatory requirements

Proper event management is the first step to ensuring that the capital requirement calculation is accurate, reliable, and aligned with regulatory standards.

Check our Help Center for more information.

Additionally, Pirani helps organizations in certifying their risk events by ensuring compliance with minimum controls and requirements for proper validation.

What Are Accounting Accounts?

Accounting accounts record and organize all financial transactions of an entity. In capital requirement calculations, they are key because they allow precise identification of revenues, losses, and other data needed to feed models like SMA (Standardized Measurement Approach), BIA (Basic Indicator Approach), and TSA (The Standardized Approach).

A well-structured accounting system guarantees traceability, regulatory compliance, and accuracy in computing the capital needed to cover risks, especially operational risk.

Without clear and up-to-date accounting accounts, it is impossible to properly support the capital requirement before regulatory authorities.

Consult our Help Center for more details.

How Does the Capital Requirement Work Under the SMA Model?

The Standardized Measurement Approach (SMA), established under Basel III, is the unique method proposed for calculating the capital requirement for operational risk. This approach replaces the three older models: the Basic Indicator (BIA), the Standardized Approach (TSA), and the Advanced Measurement Approach (AMA).

Unlike methods based on internal models, SMA offers a simpler, more comparable, and consistent approach, while maintaining risk sensitivity.

How Is It Calculated?

The SMA combines two main components:

Business Indicator (BI): An aggregated financial indicator derived from accounting items such as revenues, expenses, and operating margins.

Internal Loss Multiplier (ILM): A factor that adjusts the capital requirement based on the entity’s historical operational loss record over the past ten years.

This combination allows the capital requirement to reflect both the economic scale of the institution and its historical operational loss performance, providing a more robust, standardized measure aligned with real operations.

Formula:

ORC= BIC x ILM

Where:

BIC (Business Indicator Component): Reflects the business risk profile from the entity’s activity, income structure, and operational risk exposure. It is calculated as a percentage of BI using progressive scales based on BI size.

BI (Business Indicator): An aggregated metric of size and operational risk exposure. It is composed of three subcomponents

BI= ILDC + SC + FC

ILDC (Interest, Leases, and Dividends Component): Captures operational risk tied to financial margin. It includes net interest and leases (with an adjustment that takes the lesser between the absolute net interest income and 2.25% of interest‑earning assets, to limit distortions), plus dividend income.

*In Pirani, a secondary method can be selected without the adjustment, using only net interest/lease + dividend income.

Formulas:

With Cap on Earned Assets:

ILDC = min (| intereses ganados - intereses pagados|, 0.00225 x activos que devengan intereses) + dividendos recibidos

This method is the one officially recommended by Basel IV. The 2.25% cap prevents institutions with artificially low net margins (due to accounting policies, tax strategy, or atypical circumstances) from underreporting ILDC and underestimating their operational risk exposure.

Simple Method:

ILDC = | intereses ganados - intereses pagados| + dividendos recibidos

This is simpler and may be useful in regulatory transition phases or for smaller or less complex institutions. However, it may over‑ or under‑estimate risk if not validated properly against underlying assets.

SC (Service Component): Reflects operational risk from providing financial services. It captures income and expenses that cannot offset each other.

Formula:

SC = max(|OI|, |OE|) + max(FI, FE)

Where:

OI = Other Operating Income

OE = Other Operating Expenses

FI = Fee & Commission Income

FE = Fee & Commission Expenses

In Pirani, these values can be mapped automatically from accounting accounts per fiscal year. Years with SC ≤ 0 may be excluded if configured.

FC (Financial Component): Measures risk associated with market financial operations. It is calculated as the sum of absolute net gains or losses from:

-Trading book

-Banking book

The use of absolute values ensures full reflection of activity scale, avoiding offsets that understate true operational risk.

Two Methods for BIC (Business Indicator Component) in Pirani

By Marginal Brackets (Basel IV Model)

This method applies progressive marginal rates to the value of the Business Indicator (BI), meaning that the required capital increases not only in proportion to the size of the bank but also according to its economic activity as measured by the BI.

The formula is based on the following official brackets established by Basel:

These amounts are originally expressed in euros. In Pirani, they can be parameterized to match the local currency and country-specific regulatory policy.

The formula for each bracket is based on the data provided in the table above.

By Flat Rate:

Applies a single percentage to the total value of the BI, regardless of its size.

Useful during regulatory transition phases or in cases where the local authority allows its use.

Simplifies the calculation, although it may be less precise as it does not take progressive tiers into account.

ILM (Internal Loss Multiplier)

An adimensional factor that adjusts the required capital by operational risk, based on a bank’s actual internal operational losses.

- If historical losses are high relative to BIC, ILM > 1, increasing capital requirement.

- If losses are low, ILM < 1, reducing the capital requirement moderately.

- If sufficient historical data are lacking, ILM = 1 (no adjustment).

Formula:

LC (Loss Component)

The aggregated measure of historical operational losses used in ILM calculation. By Basel definition, LC is set as 15 times the average annual operational loss over the past 10 years (after recoveries).

Formula:

Under SMA, the LC component can be calculated applying operational event exclusion rules as allowed by local regulations. Pirani allows configuration of two exclusion mechanisms:

Individual exclusion by minimum amount:

Automatically excludes events whose gross loss amount is below a user‑defined threshold. Useful in jurisdictions where regulators allow discarding minor events to reduce statistical distortion.

Exclusion by category and aggregated minimum amount:

The user selects a hierarchical category (e.g. event type, location, process) and a minimum amount.

If the total gross losses within that category in a year exceed the threshold, that category is included in the LC calculation as a single event.

If it does not exceed the threshold, all events in that category are excluded.

If both exclusion methods are activated, the system always applies the individual amount exclusion first, and among the excluded events, it then applies the category exclusion.

How Does the Capital Requirement Based on the BIA Model Work?

The BIA Model (Basic Indicator Approach) is the simplest method to determine regulatory capital for operational risk. This model is based on the size and complexity of the business, using the entity’s gross income as the main indicator.

The approach is based on the idea that the larger and more complex a business is — that is, the higher the volume of operations and income it manages — the greater its exposure to operational risk.

To calculate the capital that must be reserved, the model takes the annual gross income (before deducting expenses, i.e., before taxes, provisions, or operating costs) and applies a fixed percentage established by regulation.

In general terms:

α = Regulatory Coefficient Set by Basel: α = 15% or 0.15

Configurable in Pirani.

GI = Average of positive gross incomes from the last 3 years.

GI = Annual Gross Income. Sum of operating income minus directly related operating expenses.

Thus:

The size of the business is measured through its gross income.

The required capital is determined by applying a fixed percentage (α) to that income.

The model does not distinguish between types of activities nor consider internal control levels or specific exposure, which makes it simple but also less precise.

How does the capital requirement based on the TSA model work?

The TSA (The Standardized Approach) is a method defined by Basel II to calculate the capital requirement for operational risk.

This model aims to improve precision compared to the BIA (Basic Indicator Approach), recognizing that different types of banking activities present different levels of exposure to risk.

Instead of applying a single percentage over total income (as in BIA), TSA divides the bank’s activities into eight business lines and applies specific weighting factors (β) to the gross income of each.

General TSA Formula

Where:

GIᵢ = Gross Income of the business line (operationally assigned)

βᵢ = Regulatory coefficient assigned to each line. Configurable in Pirani

i = Corresponding to each Business Line.

Weightings (β) per Business Line according to Basel II

|

Business Line |

β (Weighting) |

|

Corporate Finance |

18% |

|

Trading and Sales |

18% |

|

Retail Banking |

12% |

|

Commercial Banking |

15% |

|

Payment and Settlement |

18% |

|

Agency Services |

15% |

|

Asset Management |

12% |

|

Retail Services |

12% |

Is this functionality not yet active in your organization?

To activate it in your account, you need to request it.

Schedule a demo and learn how to activate it!